Insurance: A Brief History Lesson

by Loretta Gillespie

We all know that if we belong to a large enough group, then our premiums go down accordingly due to the fact that all members share in the risk. What is good for one of us, is good for all because we each depend on the participation of each other. Of course, we have to go forward on the premise that we are all honest and will conduct ourselves with ethical behavior.

Beginnings

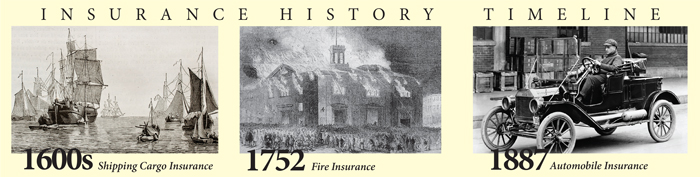

The concept of insuring items, vessels or any property of value is not new. It began in ancient times. One of the first known groups to pool their resources for the purpose of insuring it against the elements were Oriental merchants who sent their sailing vessels into harm’s way along trade routes filled with various hazards.

Often times they would send out an armada of ships to divide the chances of one holding all the cargo being sunk. In later years this came to be known as marine insurance, and now encompasses other types of insurance, including property and casualty coverage. Nowadays, property owners buy into ‘group policies’ extending their options and pooling the risks over a large group of investors. Underwriters and insurance companies collect premiums from a large group so that the burden on one person, or entity, is shared. We call this ‘the business of insurance’.

The precursor of what we know as ‘insurance underwriting’ came into practice in England in the 17th century when a group of individuals agreed to act as ‘guarantors’ for others involved in shipping cargoes from one continent to another. For a fee, they would take on the monetary risks and if nothing untoward happened to the cargo, that fee became their profit.

Most people will be familiar with one of the charter members of this group – Edward Lloyd, who was only a coffee shop proprietor at the time. That group of coffee drinkers eventually became known as Lloyd’s of London. You may associate this name with movie stars, like Angie Dickenson, who insure their image with Lloyd’s of London. This prestigious group has become famous for taking on virtually any sort of risk.

Soon another type of insurance, fire, was instituted because of several devastating losses in England. The name Nicholas Barbon is associated with the first fire policies which were sold as stocks in a company called the Fire Office.

Meanwhile, in a burgeoning country called America, other investors tried to introduce the practice in 1735. However, that first group failed within five years. A young entrepreneur by the name of Benjamin Franklin eventually started the ball rolling by forming the Philadelphia Contributionship for the Insurance of Houses from Loss by Fire, in 1752. (Sometimes referred to as Hand in Hand, in relation to it’s logo of a firemark, which was placed on houses insured by the company). Even today, the predecessor of that company continues to do business.

Meanwhile, in a burgeoning country called America, other investors tried to introduce the practice in 1735. However, that first group failed within five years. A young entrepreneur by the name of Benjamin Franklin eventually started the ball rolling by forming the Philadelphia Contributionship for the Insurance of Houses from Loss by Fire, in 1752. (Sometimes referred to as Hand in Hand, in relation to it’s logo of a firemark, which was placed on houses insured by the company). Even today, the predecessor of that company continues to do business.

Flash forward to more recent times. Henry Ford’s invention of the automobile created yet another type of need – auto insurance. In 1887, the first policy was bought by Gilbert Loomis (actually this policy was tailored from a previous policy designed for horse-drawn conveyances). Loomis purchased his policy for $7.50. It promised him $1,000 in liability coverage in the event of an automobile accident.

Insurance was catching on. People began to insure other possessions – policies like the original marine contracts were adapted to offer coverage for a multitude of other things – acts of God, or ‘natural disasters’ were now insurable. Theft and negligence were also covered. As technology advanced to air travel, oil exploration and the race for space, insurance policies followed close behind.

Today, our multifaceted economy would not be possible without the protection provided by insurance for our belongings, automobiles, homes and businesses. Natural disasters, theft, fire and accidents occur somewhere every day. A free-enterprise society could not function without protection for everything from huge industrial complexes, hospitals and schools to the homes along your street. Ultimately, all of these property owners must be responsible for taking the necessary steps in securing coverage for their own individual needs based on an assessment of the risk involved. For example, a homeowner would hardly need malpractice insurance.

Functions of Property/Casualty Insurance

It’s hard to imagine how we could pay high prices for automobiles, homes and health without the benefit of insurance to provide peace of mine and to protect us against a myriad of disasters that could literally wipe out everything we have worked for.

Purpose of Insurance

Actually, the real purpose of insurance against the loss of our property is to transfer the risk of loss to a company, rather than absorb it ourselves. In return for our premium payments, they guarantee to pay the owner to replace the loss of our homes, automobiles, boats and even our lives.

Spreading the Risk

Of course, this involves dividing that risk over a large group of people, each of who shoulder only a small portion of the amount of the replacement cost. The more people involved – the less it costs each one, resulting in the ability of the insurance companies to calculate the overall risk and the cost of each individual policy.

How Insurance Benefits Society

Our world relies on insurance. We, the individual policy owners, support the whole foundation of the premise of insurance. As such, we are actually major investors who supply the capitol on which the company runs.

To get this article and more valuable consumer information, please sign up for our FREE Premiere Edition of AWARE!™ download.

No comments yet.